For high-net-worth and accredited investors, the search for stable, passive income often leads beyond the traditional stock and bond markets. While public equities offer growth potential, they are inherently volatile. Traditional fixed-income investments, such as municipal or corporate bonds, often fail to outpace inflation or meet aggressive income targets. This dynamic has driven a significant surge in alternative investments, particularly in the realm of private credit.

One of the most compelling segments within private credit is private mortgage investing. By acting as the bank, capital investors can earn consistent, attractive yields secured by real, tangible assets.

In this ultimate guide, we will explore what private mortgage investing is, how it works, the benefits it offers, and how accredited investors can leverage this strategy to build a resilient, passive income portfolio

What is Private Mortgage Investing?

At its core, private mortgage investing involves providing capital to real estate borrowers—typically investors, developers, flippers, or commercial property owners—in exchange for regular interest payments. Instead of purchasing physical real estate and dealing with the headaches of property management, you are purchasing the debt secured by the real estate.

In a typical transaction, a private lender originates a short-term loan (often called a bridge loan) to a borrower who needs fast, flexible financing that traditional banks cannot provide. These loans are typically used to acquire, renovate, or stabilize an investment property. The loan is secured by a first-lien position on the property, meaning that if the borrower defaults, the lender has the legal right to foreclose on the asset to recover their capital.

Private mortgage investing allows individuals to participate in this lucrative market. By allocating capital to these loans, investors receive a fixed rate of return, generating passive income without the responsibilities of being a landlord.

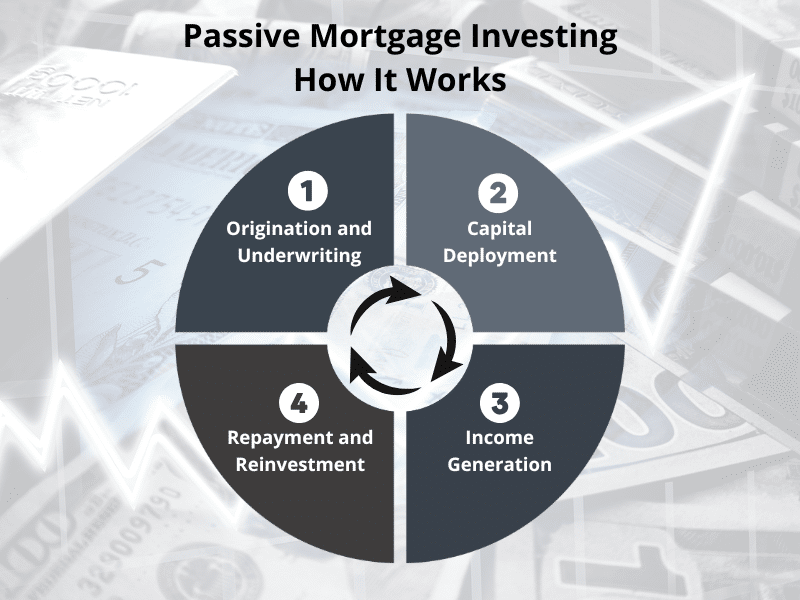

The Mechanics: How Private Mortgage Investing Works

Understanding the mechanics of private mortgage investing is crucial for evaluating its fit within a broader investment strategy. The process generally follows a structured lifecycle designed to protect the investor’s principal while generating yield.

1. Origination and Underwriting: A borrower approaches a private lending firm with a real estate project. The firm conducts rigorous underwriting, evaluating the borrower’s track record, financial health, and the underlying property’s value. A critical metric here is the Loan-to-Value (LTV) ratio. Conservative lenders typically cap the LTV at 65%, ensuring there is a significant equity cushion in the property to protect the loan.

2. Capital Deployment: Once the loan is approved, capital is deployed to fund the project. Accredited investors provide this capital, either by funding a specific loan directly or by investing in a diversified portfolio of mortgage loans managed by an experienced operator.

3. Income Generation: The borrower makes regular (usually monthly) interest payments to the lender. These payments are then distributed to capital investors, creating a steady stream of passive income. Because these are typically short-term loans lasting 6 to 24 months, the capital is relatively liquid compared to long-term equity investments.

4. Repayment and Reinvestment: At the end of the loan term, the borrower repays the principal, usually through the sale of the renovated property or by refinancing with a traditional, long-term mortgage. The investor’s original capital is returned, which can be reinvested into new opportunities to continue compounding returns.

Key Benefits for Accredited Investors

Private mortgage investing has grown rapidly as an alternative asset class because it addresses several key objectives for accredited investors and high-net-worth individuals: capital preservation, consistent income, and portfolio diversification.

1. Attractive, Predictable Yields

In today’s economic environment, finding reliable yield is challenging. Private mortgage investments frequently target annualized returns in the 10% to 12% range. Because the interest rates on these loans are fixed, the income generated is highly predictable, making it an excellent tool for funding retirement lifestyles or meeting specific cash flow needs.

2. Asset-Backed Security

mortgages are secured by a hard asset: real estate. If a borrower fails to meet their obligations, the lender holds a first-lien position on the property. This legal standing allows the lender to foreclose, take possession of the property, and sell it to recover the invested capital. When paired with conservative LTV ratios, this collateralized structure significantly mitigates downside risk.

3. True Passive Income

Direct real estate ownership is rarely truly passive. Being a landlord involves late-night maintenance calls, tenant disputes, and ongoing property management expenses. Private mortgage investing eliminates these operational headaches. Investors act strictly as the capital provider, earning returns while the borrower or a professional management team handles the heavy lifting of real estate development.

4. Portfolio Diversification

A well-constructed portfolio requires non-correlated assets–investments that do not move in tandem with the broader stock market. Private mortgage investments are insulated from the daily volatility of Wall Street. Their performance is tied to the localized real estate market and the specific borrower’s ability to execute their business plan, providing a robust hedge against public market downturns.

5. Shorter Investment Horizons

Many alternative investments, such as private equity or venture capital, require investors to lock up their capital for five to ten years or more. Private mortgage loans, particularly bridge loans, are typically short-term in nature. This 6-to-24-month lifecycle provides investors with a quicker return of principal, allowing for greater flexibility to adjust their investment strategy as market conditions change.

Comparing Private Mortgages to Other Real Estate Investments

When evaluating real estate opportunities, investors often weigh private mortgages against other popular vehicles, such as Real Estate Investment Trusts (REITs) or direct equity ownership.

| Investment Type | Income Predictability | Asset Security | Volatility | Management Required |

| Private Mortgage Investing | High (Fixed Interest) | High (First-Lien on Real Estate) | Low | None (Passive) |

| Equity REITs | Variable (Dividends) | Moderate (Corporate Ownership) | High (Publicly Traded) | None (Passive) |

| Direct Real Estate Ownership | Variable (Rent minus Expenses) | High (Direct Ownership) | Moderate | High (Active) |

As the table illustrates, private mortgage investing occupies a unique middle ground. It offers the hard-asset security of direct ownership but with the passivity of a REIT, all while providing highly predictable income insulated from stock market swings.

Who Qualifies for Private Mortgage Investing?

Due to regulatory guidelines set by the Securities and Exchange Commission (SEC), many private mortgage investment opportunities are restricted to accredited investors.

To qualify as an accredited investor in the United States, an individual must meet at least one of the following criteria [1]:

- Have an earned income exceeding $200,000 (or $300,000 together with a spouse) in each of the prior two years, with a reasonable expectation of the same for the current year.

- Have a net worth over $1 million, either alone or together with a spouse, excluding the value of their primary residence.

- Hold certain professional certifications, designations, or credentials in good standing, such as a Series 7, Series 65, or Series 82 license.

These regulations ensure that investors participating in private markets have the financial sophistication and capacity to bear the associated risks.

Mitigating Risk: What to Look for in a Lending Partner

While private mortgage investing offers significant benefits, it is not without risk. The primary risk is borrower default. Therefore, the success of this strategy relies heavily on the expertise and discipline of the lending partner or operator originating the loans.

When evaluating a private mortgage opportunity, consider the following:

- Underwriting Standards: Does the lender require strong borrower credit, extensive real estate experience, and significant personal financial guarantees?

- Conservative Leverage: Are loans capped at a reasonable Loan-to-Value (LTV) ratio (e.g., under 65%) to ensure a margin of safety if property values decline?

- Track Record: Does the lending team have a proven history of successfully navigating different market cycles and recovering capital in the event of a default?

- Market Focus: Does the lender operate in economically resilient markets with strong demand and limited supply, such as Hawaii or other robust regional hubs?

Conclusion

For accredited investors seeking to diversify their portfolios, reduce public market exposure, and generate reliable cash flow, private mortgage investing represents a powerful strategy. By transitioning from an equity owner to a debt provider, investors can secure their capital against tangible real estate assets while earning attractive, fixed-income yields.

At Myers Investment Group, we specialize in providing accredited investors with access to institutional-quality private mortgage opportunities. With a focus on disciplined underwriting, capital preservation, and transparent communication, we help our clients build wealth securely through real estate-backed passive income.

Ready to explore how private mortgage investing can enhance your portfolio? Schedule a suitability call with our team today to discuss your financial goals and view our current investment opportunities.

Copyright 2026: Myers Investment Group